now loading...

“The market is euphoric, complacent, but nervous,” remarked a fixed-income sales executive in January 2020. But even with 2019’s buffet of high-yield issuance on display before hungry investors, some were nervously wondering if the trend would continue.

The Covid-19 pandemic confirmed their fears. Soon after its outbreak, all corporate bonds dived deeply and safe-haven asset prices skyrocketed. The 30-year Treasury price swung up from 99 in February to over 120 during the March sell-off. Yet the market quickly turned around and has been gathering momentum since April.

Source: S&P Capital IQ

Source: S&P Capital IQ

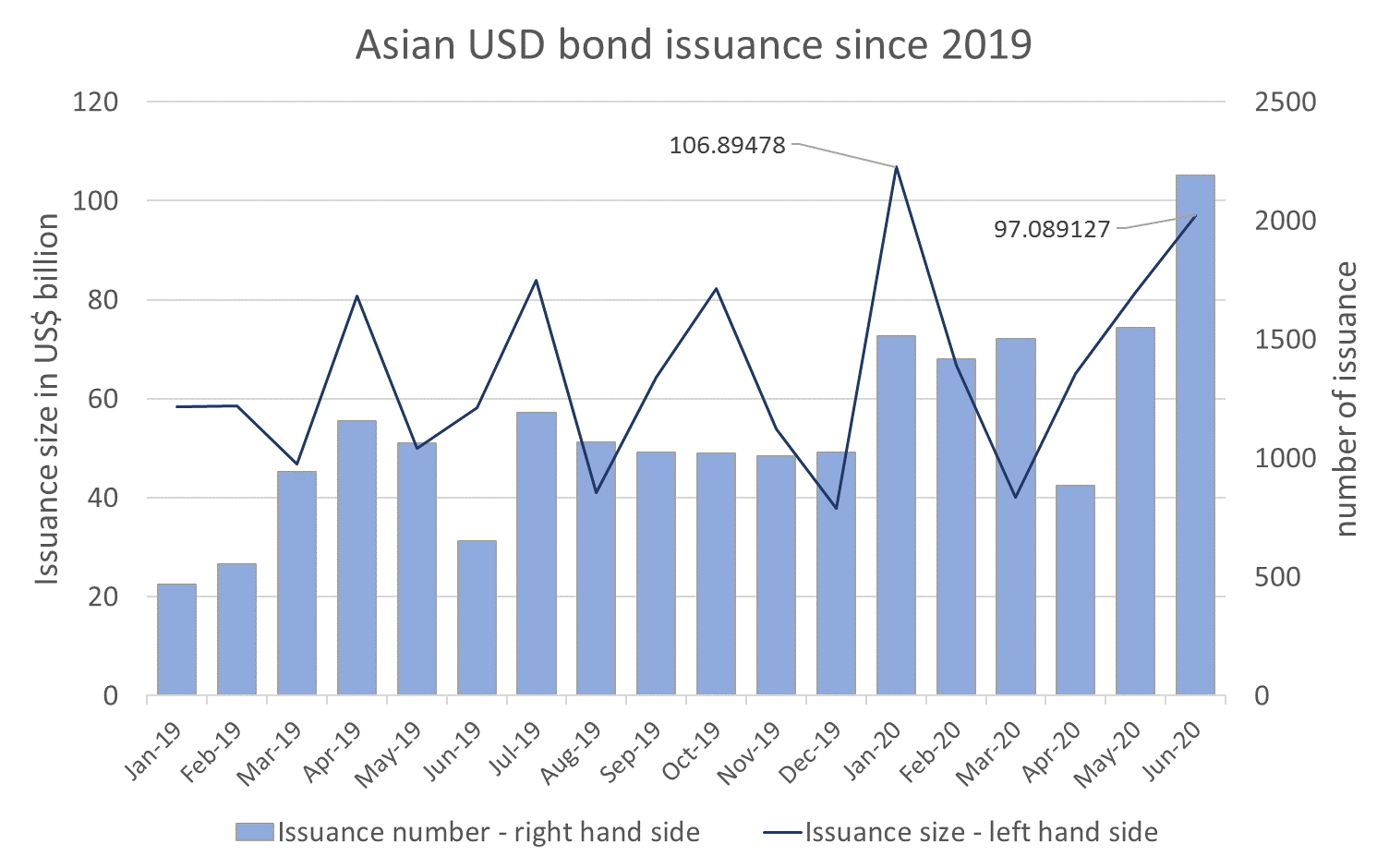

Figures supplied by S&P Capital IQ show US dollar bond issuance out of Asia amounted to US$106 billion in January, a record monthy high when compared with 2019. Despite the March figure dropping to its lowest level at US$ 40 billion, issuance rebounded immediately in April and reached US$97 billion in June, recording the second-highest monthly level over the past year.

Though the excitement has returned to the market, investors can’t be as complacent as they were in 2019. The level of high-yield issuance dropped 34.1% to US$34.62 billion, compared with US$52.51 billion during the January-to-June 2019 period, according to Refinitiv figures. In particular, some of the attractive Chinese property names like China Jinmao Holdings Group and China Resources Land have not tapped the bond market in the first half of 2020. A contributing factor to the lower issuance level from the Chinese property sector was the introduction by China’s National Development and Reform Commission of new requirements on the use of proceeds for refinancing.

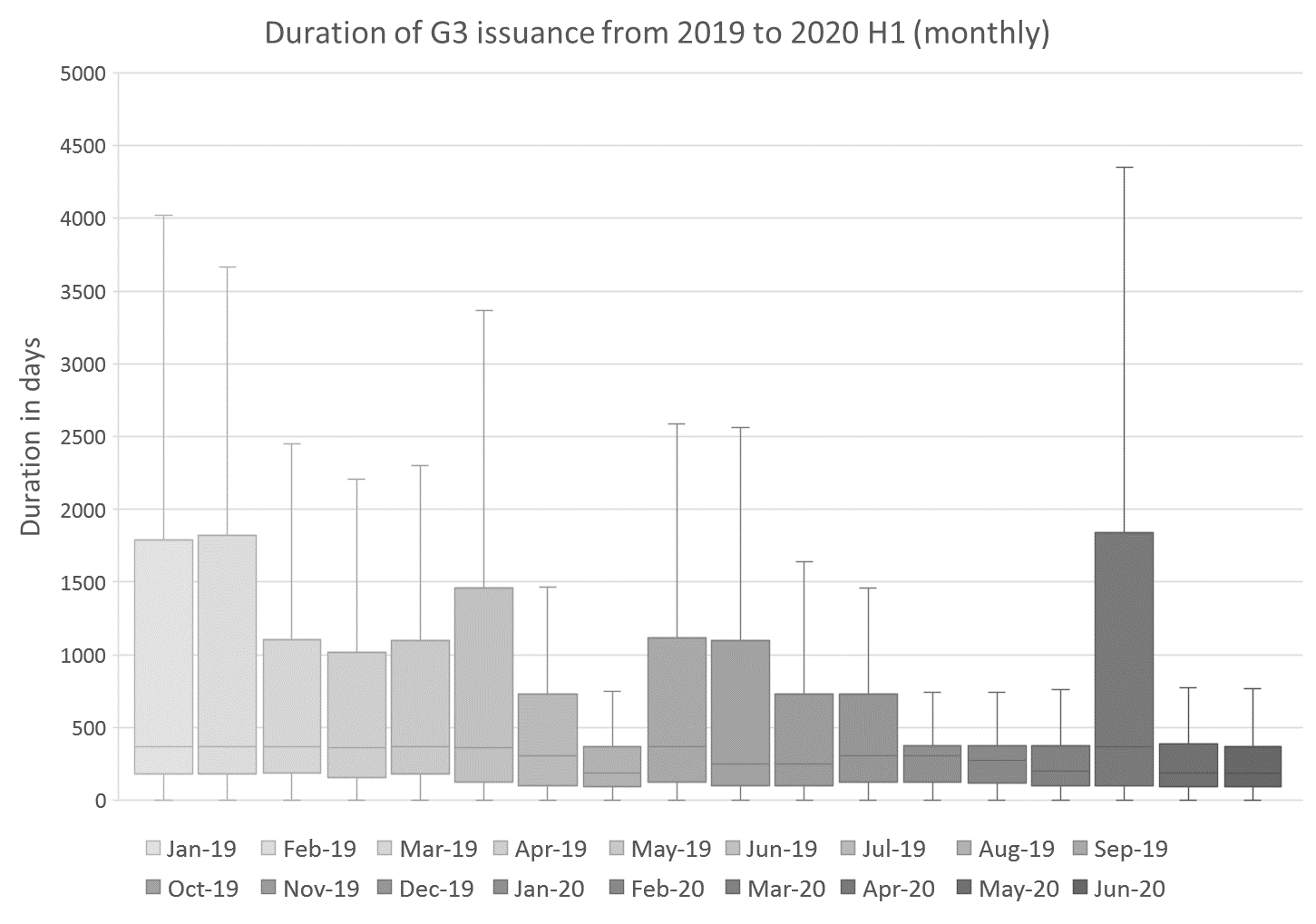

Apart from the subdued high-yield issuance, investors are also facing shorter-duration issuance. According to S&P Capital IQ’s figure, the average issuance duration in the first half of 2020 was 910 days, compared with 1238 days in the same period last year. The anomaly in April, shown in the chart below, can be attributed to bigger-sized and longer-tenor issuance like the 6.2 times oversubscribed deals issued by PETRONAS and the first-ever 50-year bond issued by the Republic of Indonesia.

Source: S&P Capital IQ

Source: S&P Capital IQ

Faced with shorter-duration and lower-yield issuance, investors have rebalanced their portfolio more frequently and searched for valuable credits in the secondary market. The renewed appetite for riskier assets has contributed to rising bond prices. For example, KAISAG 11.950% 12Nov2023 Corp ( USD ), CENCHI 7.900% 07Nov2023 Corp ( USD ), and FTHDGR 12.250% 18Oct2022 Corp ( USD ) are now all trading above pre-pandemic levels. Bond issues from other notable names like Agile and Evergrande are also trading close to pre-pandemic levels, having rebounded strongly from their lows in March.

The robust demand in the secondary market has led to heightened competition among brokerage houses and investment banks. Amid this growing competition, The Asset Benchmark Research has launched its Asian G3 Bond Benchmark Review 2020. This annual survey provides a great opportunity for sell-side firms to boost their market-making credentials.

Investors have a chance to recognize the best sell-side individuals ( analysts, economists, strategists, sales reps, and traders ) who have delivered extraordinary services over the last 12 months. For more details, please click here.