now loading...

Holding power and ensuring that you have enough cash on hand, that is the important mindset many businesses are having in today’s difficult economic environment amid the Covid-19 pandemic.

With profits falling and revenues uncertain, treasury management professionals such as CFOs and treasurers are being given the tough task of ensuring their respective businesses have enough resources available to keep afloat.

These were some of the sentiments picked up by the Asset Benchmark Research’s ( ABR ) annual Treasury Review Survey 2020 during the first half of this year, when Covid-19 cases started to pick up globally.

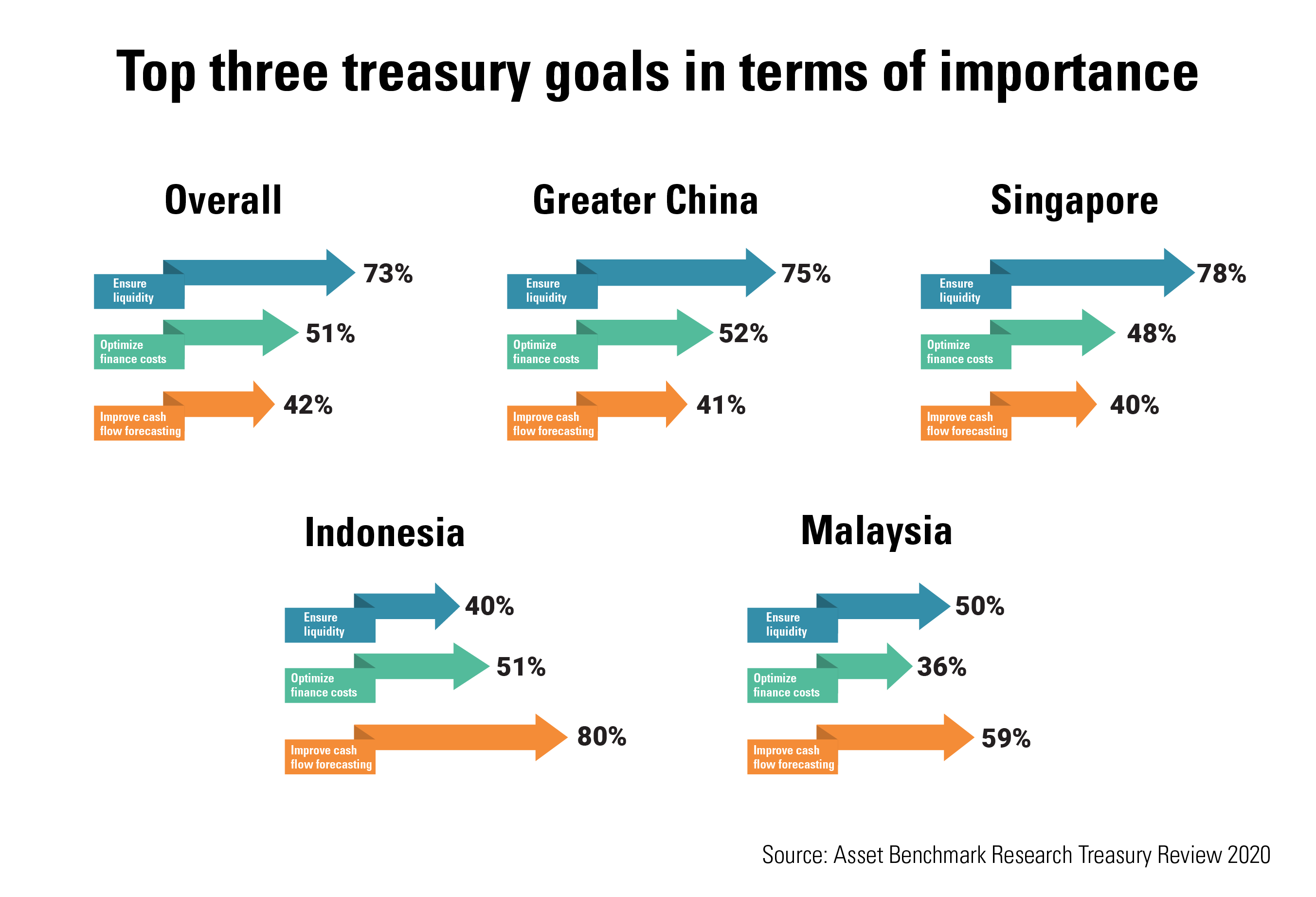

For many survey participants, ensuring liquidity was a key objective they wanted to achieve against the new normal of the pandemic. In fact, 72% of businesses surveyed cited ensuring liquidity as a top three-treasury goal followed by optimizing financing costs ( 51% ) and improving cash flow forecasting ( 42% ).

The current primary focus on effectively handling liquidity has prompted treasury professionals to self-reflect and examine areas that could be improved within their organizations. These include finding hidden pockets of liquidity through account rationalizing or leveraging on virtual accounts for payables/receivables to improve overall reconciliation.

Exploring additional areas of financing, with an aim to free up capital was another area treasury professionals could examine further. For example, 75% of respondents from the ABR’s Treasury Review 2020 cited an enhancement in liquidity due to implementing supply chain finance programmes.

While there are clear benefits of such a financing arrangement, just less than half ( 44% ) respondents did not have one in place but expressed interest in supply chain financing solutions in the near-term future.

Better treasury management coordination in the form of increased centralization overall is also what is needed to get a better handle of a company’s finances. In Asia, a number of businesses have made attempts to setup regional treasury centres in Hong Kong or Singapore due to their advanced market infrastructure and market liquidity.

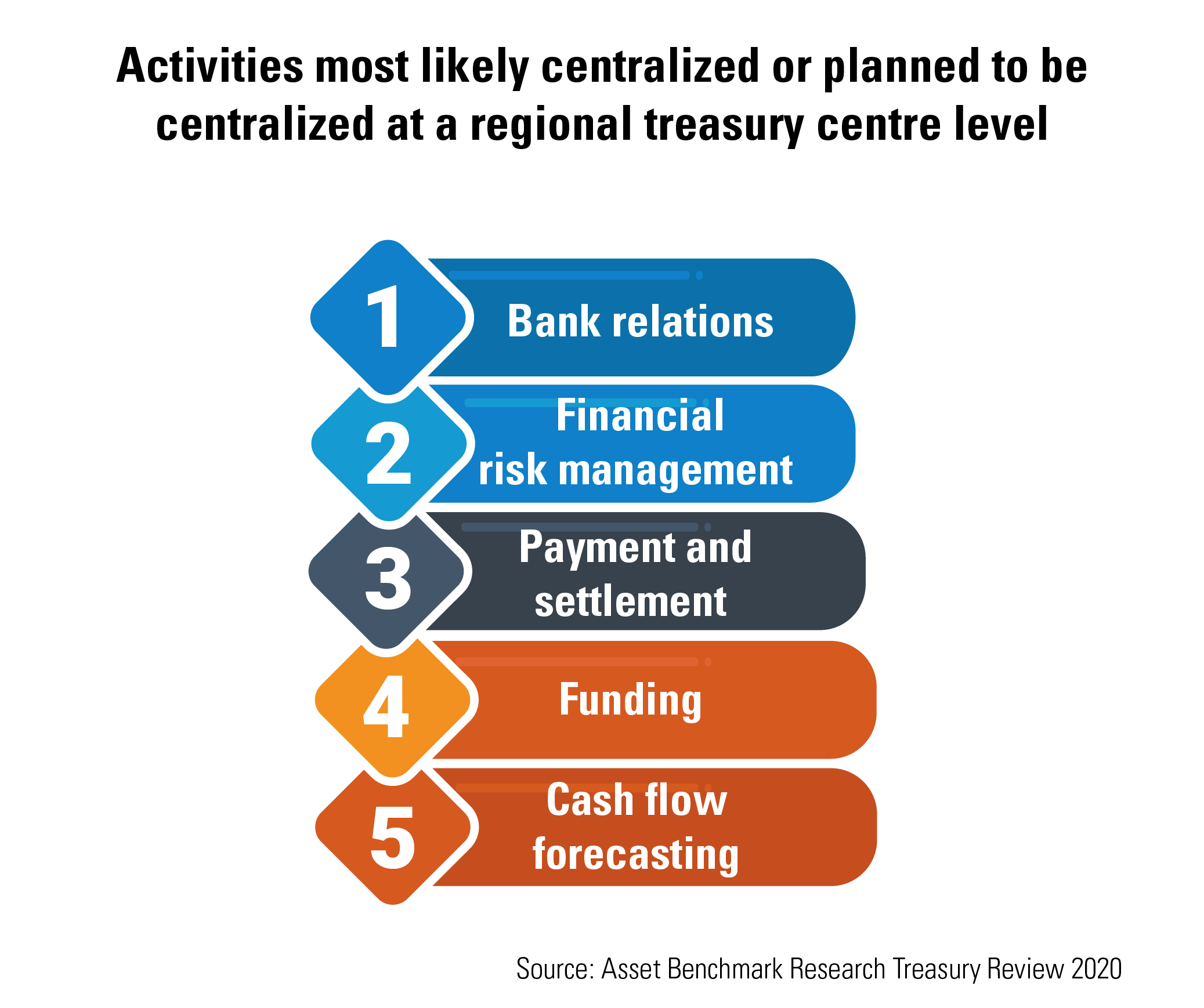

According to data from ABR’s Treasury Review 2020, respondents were more likely to centralize the coordination of banking relationships ( 70% ) and financial risk management ( 65% ) rather than liquidity management ( 41% ) which ranked seventh in terms of centralization priority. Indicating that there is still headroom for businesses to strategically manage their liquidity.

“We are trying to have a centralized approach as much as we can. I think centralization actually works. Every organization has a core business and you don’t want to contaminate the core business with a supporting activity. If you were not centralized, then you wouldn’t have every single business unit focusing on their core business,” highlights a treasurer from a logistics company. “One thing I have learned from this Covid-19 situation is that cash is king and that we need to protect our assets. You don’t know what impact this Covid-19 is going to have on your business.”

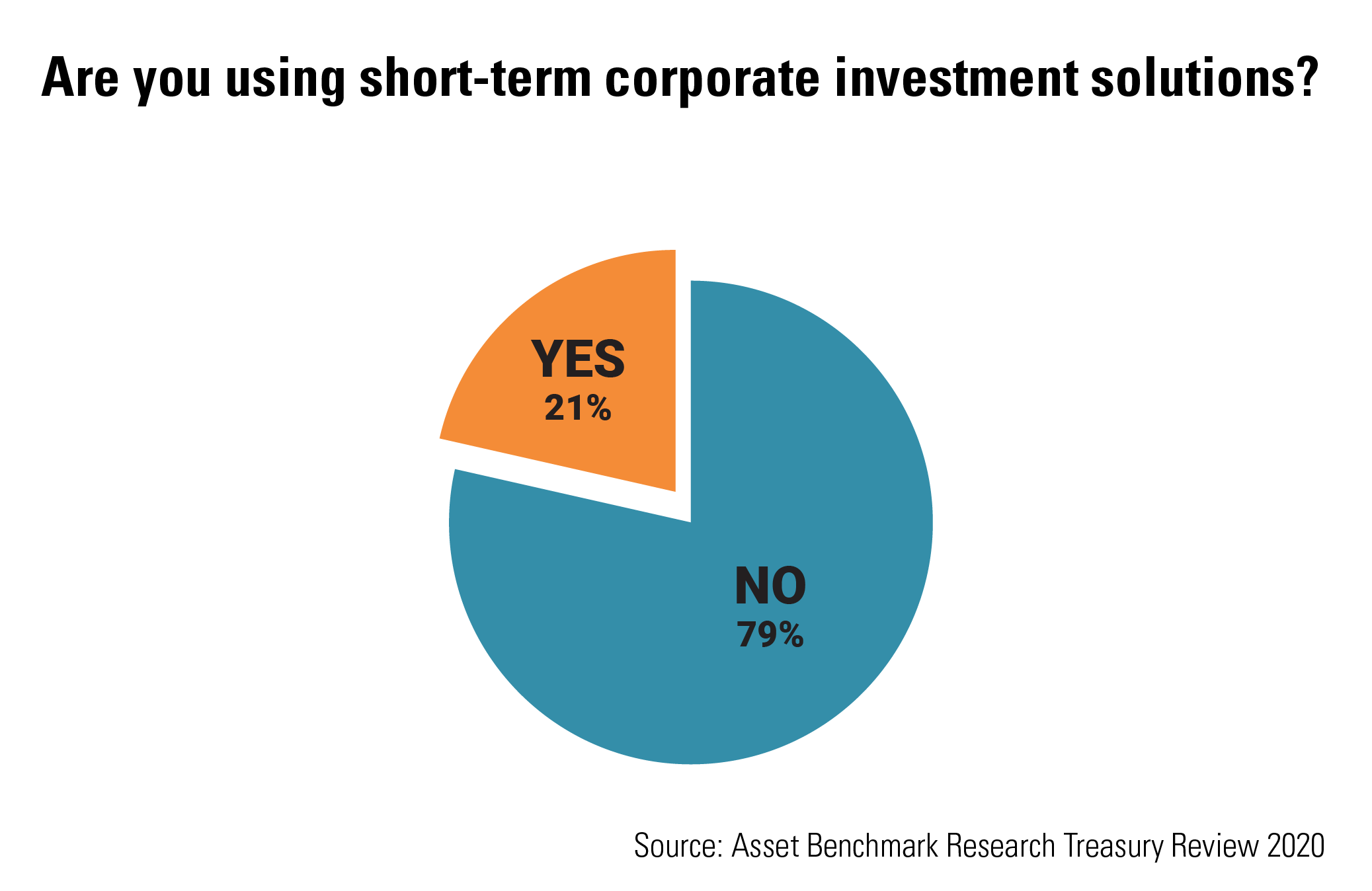

This need for cash on hand has evidently put a damper on firms offering short-term corporate investment solutions such as money market funds. ABR data reveals that 79% of participants are not currently using such investment solutions, showing that businesses are quite content to keep their funds in regular deposit accounts despite the low interest rates.

About Asset Benchmark Research’s annual Treasury Review

Conducted since 2013, ABR’s Treasury Review surveys corporates across Asia on an annual basis to understand the challenges faced by corporate treasurers and CFOs and the solutions they consider best suited to navigate financial markets. In 2020, around 700 corporate finance representatives participated in the survey, led by financial decision-makers in Greater China, India and Singapore. Based on annual turnover, 47% of respondents are small and medium-sized enterprises ( less than US$250 million turnover per annum ), 21% are mid-caps ( US$250 million to US$1 billion turnover per annum ) and 32% are large corporations ( more than US$1 billion turnover per annum ).