now loading...

Despite the pressing need for CFOs and treasurers to reduce debt on their balance sheet and improve their relationship with counterparties, some companies are still unaware of or uninterested in supply chain finance solutions.

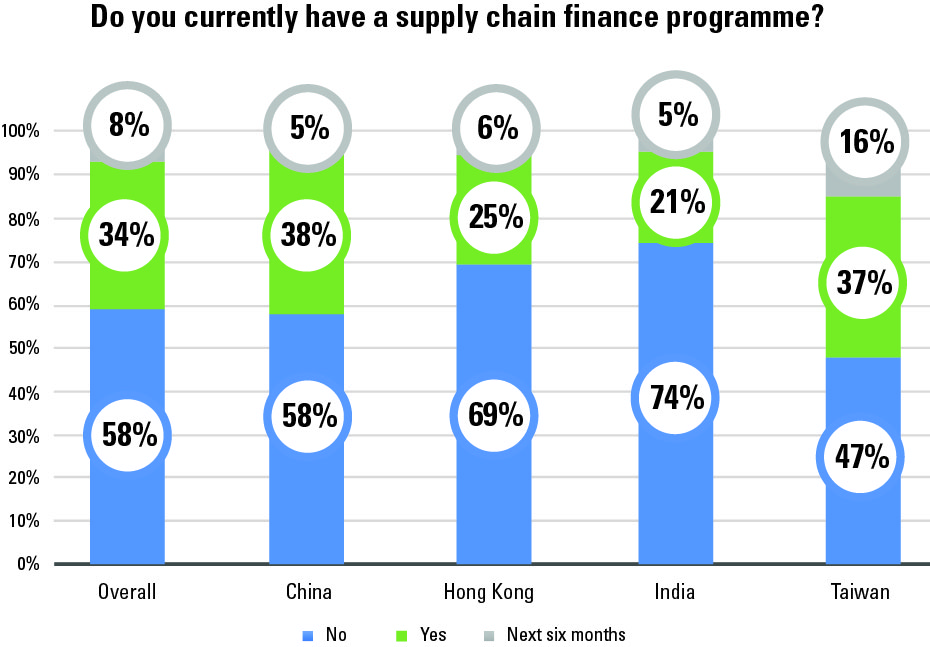

This is according to Asset Benchmark Research (ABR) 2019 Treasury Review, which found that 58% of survey participants didn’t have either a buyer finance or supplier finance process in place with a bank. Moreover, only 8% of participants were thinking about implementing a supply chain solution in the next six months.

This is a worrying sign given that there is a growing trade finance gap in Asia. In 2017, the Asian Development Bank estimated that gap to be US$1.5 trillion with the lack of working capital for SMEs as the main reason behind this.

The lack of awareness of such financing solutions is an opportunity for service providers which have been looking to provide banking services for the entire ecosystem of their client from supplier to distributor.

Using technology tools such as big data, global banks such as Standard Chartered have been diligently combining the datasets of their commercial bank and corporate bank divisions so that suppliers or distributors within the bank’s network could be easily onboarded to a particular supply chain finance programme.

ABR has gathered from several interviews during the surveying period that the onboarding process of counterparties was a difficult element companies faced when setting up a supply chain finance program.

“We wanted a financing solution which was fully compliant with the current regulatory framework and which also met our requirement of unlocking debt on our books,” explains an India-based textile manufacturer, which recently embarked on their first supply chain finance solution. “We also wanted a solution which would not interfere with our regular finance operations.”

Other areas of big data usage point to being able to give clients a better insight into whether their cash conversion cycle of days sales outstanding is below or better than industry peers. Data from the 2019 Treasury Review reveals that a service provider’s ability to give big data working capital insights was the top digital service reason to work with a bank.

Regarding the participants that had a supply chain finance programme, many of them shared that they were happy with the enhancement of liquidity within their organization followed by having extended payment terms. Large companies were more content with extending their payment terms while small and medium enterprises were glad to have additional liquidity.

The financial controller of a Malaysian-based consumer goods company was particular pleased with the firm’s supplier finance solution, saying that “it’s difficult to get the non-recourse financing in Malaysia so our bank introduced an insurance broker to manage the risk. The local financing is a little bit more expensive than the non-recourse financing that we have.”

Companies that had a supply chain finance solution in place were more or less equally split between buyer finance and supplier finance regionally, but differed when it came to particular markets with Hong Kong-based respondents favoring buyer finance while respondents in Taiwan and India opted for supplier finance.

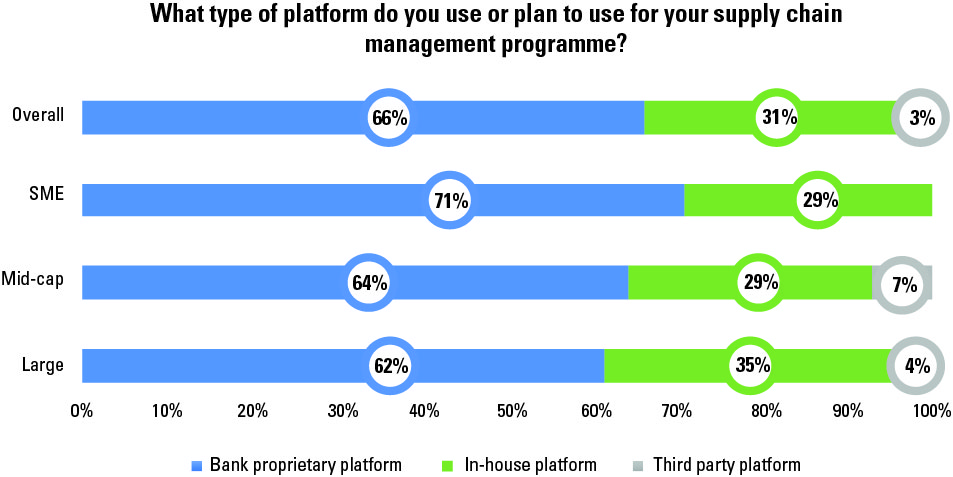

In terms of managing their supply chain finance programs, the majority (66%) of respondents were reliant on bank proprietary platforms while another 31% relied on an in-house platform.

The possible expansion of supply chain finance programs highlights the increasing importance for CFOs and treasurers to have a better visibility of the types of programs they have with their various stakeholders along the supply chain.

About Asset Benchmark Research’s annual Treasury Review

Conducted since 2013, Asset Benchmark Research surveys corporates across Asia on an annual basis to understand the challenges faced by corporate treasurers and CFOs and the solutions they consider best suited to navigate financial markets. In 2019, almost 800 corporate finance representatives participated in the survey, led by decision-makers in Greater China, India and Indonesia. Based on annual turnover, 54% of respondents are small and medium sized enterprises, 27% are mid-caps and 19% large corporations (>US$1bn turnover per annum).

View from Standard Chartered

Supply chain finance (SCF) is apparently surpassing the conventional trade finance as identified in The Asset survey. Increasingly financial institutions are adapting to the digital revolution and integration with fintechs and non-financial solutions providers, with a shift from banking the client to banking the client’s ecosystem.There is significant opportunity in SCF for financial institutions that focus on banking the Small-Medium Enterprises and mid-cap market across Asia; these institutions are well poised to meet a portion of the $1.5T SME funding gap. However, just focusing on the SME is not enough to capture the opportunity, as large corporates in the region, representing 19% of the survey respondents, are vital to the financing structure.In any SCF financing program, the large corporates drive the economics of the supply chain with their buyers and suppliers which are typically SME companies. A large corporate’s relationship with its buyers and suppliers is ultimately what a financing institutions focus on when considering an SCF programme opportunity. Once a programme is availed the large corporate will indeed see the benefits as presented in this article, however, of equal benefit is the improved liquidity that the SME buyers and suppliers also experience.While the benefits of SCF can be readily shown, there are also aspects of the practice that the financial institutions and large corporates involved should be mindful of: SCF is a great tool that can be used to provide liquidity throughout the supply chain, but there have been instances where SCF has induced liquidity stress by financing outside of industry norms. This need not cause fear, however it is important that a client understands the pro and cons of such financing programs, and that the financial institutions have right framework to assess the client intent and deal appropriateness, such as financing within the normal payment terms of the industry, program being completely voluntary for counterparties, etc.The article also highlights that some respondents were unaware or uninterested in SCF and perhaps this explains the lower rates of uptake of the structures. The benefits are compelling and financing institutions should focus on creating awareness, particularly with the large corporates who can in turn share in the benefits with their buyers and suppliers in the region, and globally.